To this point in the session, the Legislature has been basing its supplemental FY22 and FY23 budget discussions on the oil price and other revenue projections contained in the Department of Revenue’s (DOR) Fall 2021 Revenue Sources Book (Fall21 RSB), published last December.

The tenor of those discussions is about to change – or at least it should – significantly.

By March 15, DOR likely will publish its revised and updated revenue projections in the form of the Spring 2022 Revenue Forecast (Spring RF). While in most years the Spring RF contains just a few tweaks here and there, because of the huge changes in oil markets in the intervening three months since the Fall21 RSB was published, this year’s Spring RF is likely to reflect significant changes in the state’s revenue outlook.

There are a number of ways to look at the likely changes. Let’s start with a basic one, focused on comparing the prices currently prevailing in the oil futures market as of yesterday’s (Thursday, March 3) close with those on which the Fall21 RSB is based. We have also included those reflected in last Spring’s (2021) RF for perspective.

As is clear, at least looking forward over the next five years the prices currently prevailing in the oil futures market are substantially higher than those projected in the Fall21 RSB.

Even the projection for the current fiscal year (FY22), which was nearly half way done when the Fall21 RSB was published, is substantially different. Based on the realized prices since plus those currently prevailing in the oil futures market for the four months remaining, the average FY22 price which likely will be reflected in the Spring RF is now somewhere in the range of $90/bbl, nearly 20% higher than the level projected in the Fall21 RSB.

And the average price for FY23 which likely will be reflected in the Spring RF is now somewhere in the range of $93, more than 30% higher than projected in the Fall21 RSB.

These higher prices, of course, translate into significantly higher state revenues. Using DOR’s Fall 2021 Price Sensitivity Analysis as a guide we regularly estimate each Friday the traditional revenues resulting from the then current prices prevailing in the oil futures market through the period covered by the Fall21 RSB. Here is our most recent estimate, again updated through yesterday’s market close.

As noted, based on the current prices prevailing in the oil futures market, projected traditional revenues for the current fiscal year (FY22, in black) are now more than 30% higher than projected in the Fall21 RSB (red), and, for FY23, now more than 60% higher than projected in the Fall21 RSB.

For those curious, the reason the percentage increase in the projected revenues for those years is even higher than the percentage increase in the related oil price is because of the progressivity built into Alaska’s oil production tax structure. As oil prices rise – particularly as they pass $85 – the state takes in an increasingly higher percentage of the revenue/barrel. Again using DOR’s Fall 2021 Price Sensitivity Analysis as a guide, we chart that effect here.

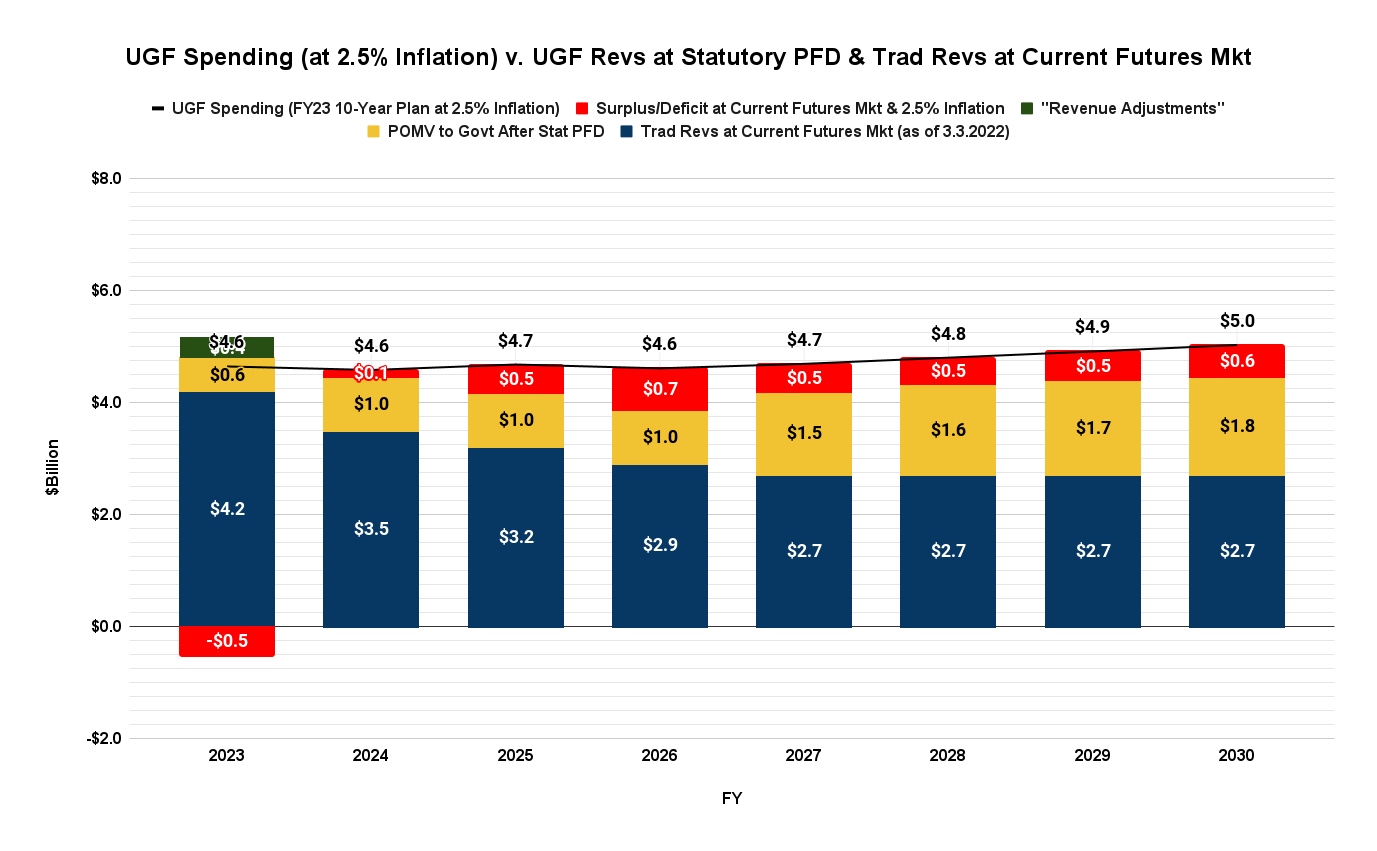

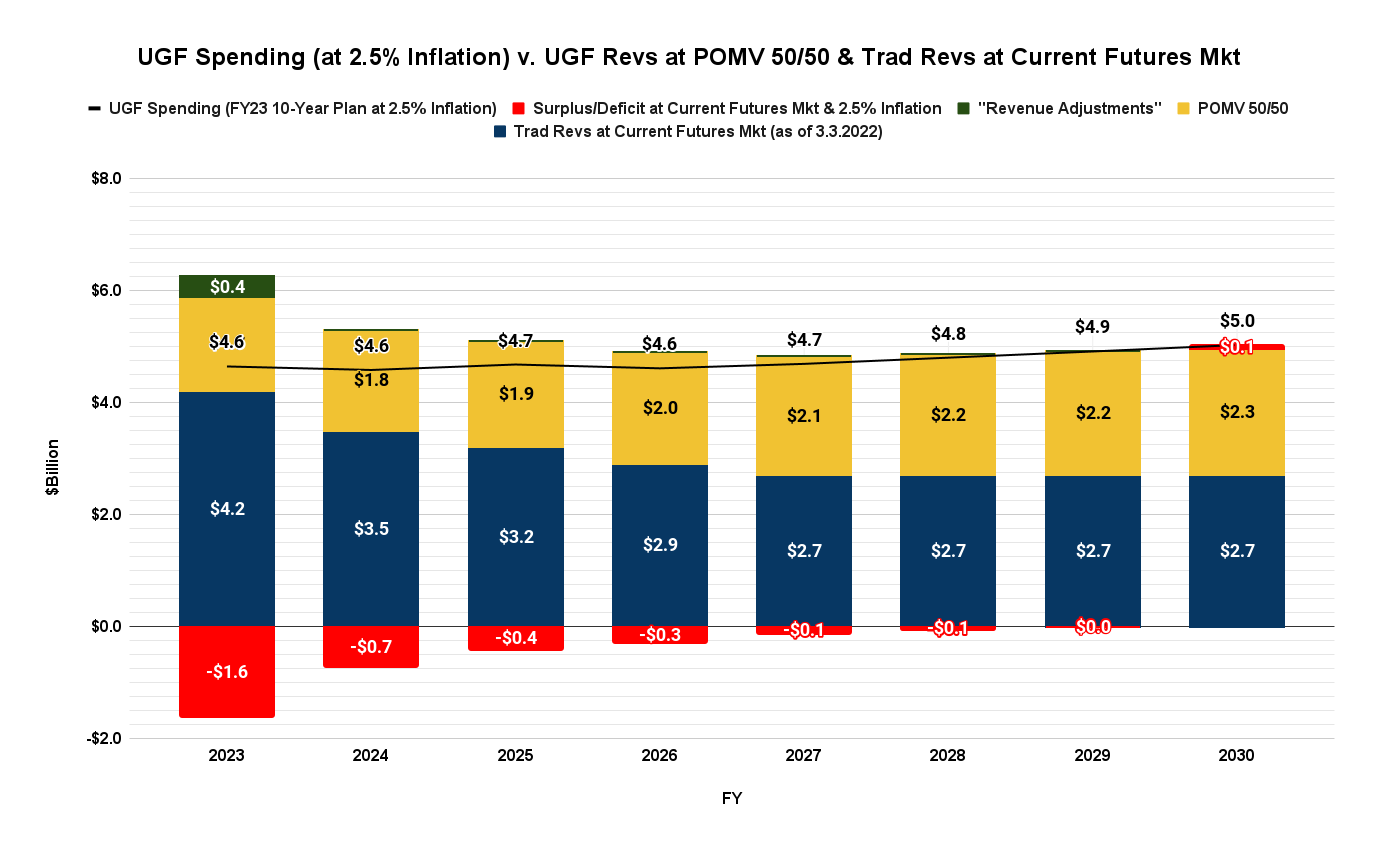

The next question, of course, is – or at least should be – “so what does that mean to the budget and 10-year outlook”?

We look at that two ways. The first is to overlay the resulting overall revenues – traditional plus the portion of the percent of market value (POMV) draw from the Permanent Fund intended for government – on the spending levels projected in Governor Mike Dunleavy’s (R – Alaska) FY23 10-year Plan, adjusted as we explained in a previous column for a realistic inflation level.

Here is the result under both current law (statutory PFD) and Dunleavy’s proposed POMV 50/50 PFD.

As is clear from the first chart, at the current price levels prevailing in the oil futures market the FY23 budget balances at the current law (statutory) PFD – in fact, produces a surplus (indicated by the portion in red below the line) – without the need to divert any revenues from the PFD to government. As the second chart indicates, for FY23 the Governor’s approach – reducing the PFD to POMV 50/50 – results in an even greater surplus.

Those relationships change over time. Even at the higher prices currently prevailing in the oil futures market and with the spending constraints proposed by the Governor, the current law (statutory PFD) budgets subsequent to FY23 continue to show deficits (indicated by the portion in red above the line) that would need to be closed in some fashion.

On the other hand, the budgets using the Governor’s approach – again, reducing the PFD to POMV 50/50 – continue to show either a surplus or, at a minimum, near balance throughout the remainder of the decade.

The second way we chart the impact of changing oil prices on the budget is to look at “breakeven” prices – what would the price of oil need to be to produce a balanced budget (i.e., break even) under various approaches.

Again, using DOR’s Fall 2021 Price Sensitivity Analysis as a guide we chart (in the solid lines) what the price of oil would need to be to produce sufficient revenues to balance the budget (i.e., breakeven) under three approaches: where there is no draw made from the Permanent Fund (blue), where the portion of the draw available to government is that provided under current law (statutory PFD, in red), and where the portion of the draw available to government is that which would be provided under the Governor’s proposal (POMV 50/50 PFD, in maroon).

Overlaid on that we include (in the dashed lines) the oil price projected in the Fall21 RSB (green) and those currently prevailing in the oil futures market (black).

From those it continues to be clear that, at the price levels currently prevailing in the oil futures market, a current law (statutory PFD) budget not only would balance (breakeven) with the spending levels projected in the Governor’s FY23 budget, it would produce a slight surplus.

And – again at the price levels currently prevailing in the oil futures market – a budget based on POMV 50/50 would produce surpluses through FY28, and even after that continue to break even, or at least come close, through the remaining two years of the decade.

These are significantly different outcomes than result from using the price projections reflected in the, now outdated Fall21 RSB. Using those, a budget based on the current law dividend would never balance, and while a budget based on POMV 50/50 would balance in FY23, thereafter it would produce growing deficits throughout the remainder of the decade.

Thus far this session, the use of the Fall21 RSB price levels have produced analysis and proposals focused on restructuring the PFD, at best, to one based on POMV 25/75 (25% of the POMV draw to the PFD, with the remaining 75% directed to government).

Even this week’s “energy relief” proposal from the House Coalition is based on POMV 25/75. While it increases the distribution for FY23 (for that single year, to a level approximating the Governor’s POMV 50/50 approach), it reverts thereafter to, presumably, the underlying POMV 25/75 approach incorporated in HB 259, which to this point has appeared to be the Coalition’s lead, long-term fiscal bill, as well as the Senate Finance Committee’s SB 200.

In short, while the proposal purports to reflect the huge change in oil prices since last December, it only does so only for one year, and then reverts back to the approaches premised on the Fall21 RSB.

Looked at from the perspective of the price levels currently prevailing in the futures market throughout the remainder of the decade, those proposals now produce huge surpluses. But unlike the “natural” surpluses built up during the period from 2008-2014 (revenue in excess of then-current law spending), these largely result from PFD cuts and, as result, are being built mostly by taking money out of the pockets of middle and lower income Alaska families.

Because they no longer are based on current oil price projections, these proposals (based on the Fall21 RSB) should quickly be set aside once the focus shifts to the substantially revised projections we anticipate will be contained in the Spring RF.

To be certain, those intent on continuing to minimize the PFD and maximize the diversion of the POMV to government – which as we’ve explained in previous columns, primarily benefits the top 20% – will likely push to maintain the focus on the numbers contained in the Fall21 RSB. But that should be viewed for what it is, a selfish attempt by the top 20% to continue to direct the earnings from the Permanent Fund to their own benefit, rather than, as intended by those who originally pushed for and adopted the PFD, sharing them equally between government and all Alaska families.

In short, in our view, the discussions going forward should give as much respect to the now, updated revenue forecasts which likely will be reflected in the Spring RF as the discussions previously this session gave to the now outdated Fall21 RSB.

Brad Keithley is the Managing Director of Alaskans for Sustainable Budgets, a project focused on developing and advocating for economically robust and durable state fiscal policies. You can follow the work of the project on its website, at @AK4SB on Twitter, on its Facebook page or by subscribing to its weekly podcast on Substack.