Regular, or even occasional, readers of this page will likely recall that, in previous columns, we have called for significant reforms to Alaska’s current oil tax approach, particularly that underlying the state’s production tax code.

The Spring 2026 Revenue Forecast (Spring Forecast) confirms that position.

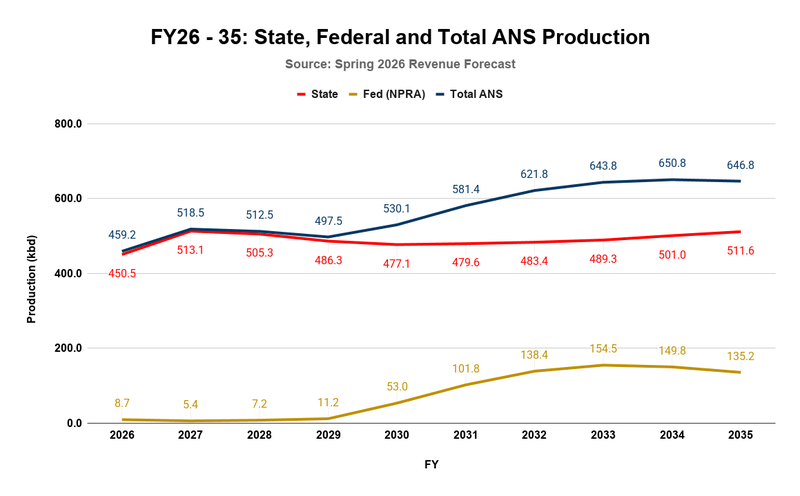

As in previous forecasts, the Spring Forecast projects significant growth in production volumes over the next ten years. Overall, Alaska North Slope (ANS) production volumes (the blue line in the following chart) are projected to rise by more than 40%, from a projected level of 450.5 thousand barrels per day (kbd) in Fiscal Year (FY) 2026 to 646.8 kbd in FY2035. While an increase in volumes from federally owned lands in the National Petroleum Reserve – Alaska (NPRA) is projected to provide the bulk of that growth, production from state-owned lands is also projected to contribute, increasing over the period by more than 13%, from 450.5 kbd in FY2026 to 511.6 kbd in FY2035.

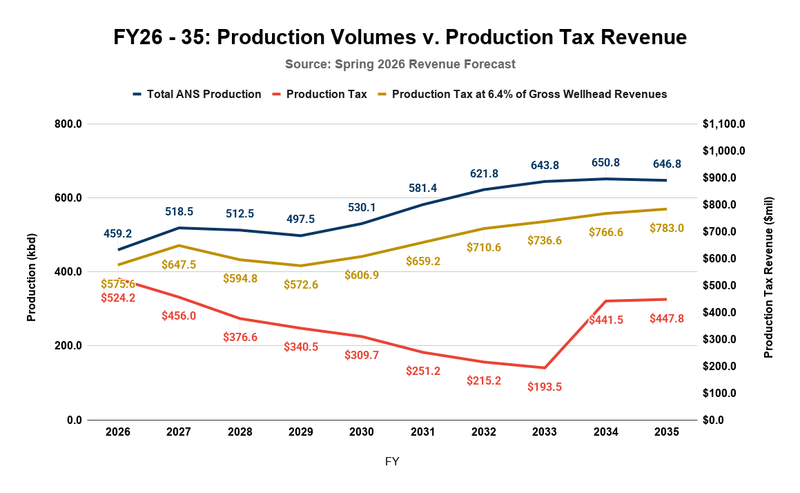

But at the same time, annual revenues from production taxes (the red line in the chart below), which apply equally to both state and federal volumes, are projected to decline precipitously, by over 50% in the first five years of the period (through FY2031), before recovering some, but still to decline by approximately 15% from where they start in FY2026, to where they end in FY2035.

During the passage of “SB 21,” the current oil tax code, in 2013, as well as during the subsequent referendum in 2014 on whether to retain the act, the proponents of the legislation argued that the significant reductions in the then-level of production taxes embedded in the act were worthwhile to Alaskans because they would incentivize additional oil development that, when it occurred, would result in commensurate increases also in state revenues from that production.

But now that we are here, with oil production growing significantly, not only are the promised revenue increases not materializing, but production tax revenues are, in fact, declining.

To correct for that failure, Alaska’s oil production tax code must be reformed to ensure the promises made in 2013 and 2014 are actually realized.

Some attempt to deflect attention from the need for reform by arguing that the decline in production tax revenues is due to changes in projected oil prices over the period. But that’s not accurate. Compared with the precipitous declines in production tax revenues, oil prices projected in the Spring Forecast decline by only 8% over the first five years and by 3% over the full ten-year period.

Instead, the real cause of the decline over the period is the drop in the share of gross wellhead revenues (net of royalty volumes) generated by production taxes, which some refer to as the “effective production tax rate.” That declines from an already-low 5.46% at the beginning of the period (FY2026) to 2.29% at the five-year mark (FY2031), before recovering slightly to 3.43% at the end of the period (FY2035).

That decline is due to how SB 21 is performing in the current environment, not oil prices.

Others argue that the decline in production taxes is acceptable because it is offset by higher revenue in other categories, such as royalties. But that’s also not accurate.

While oil production is projected to increase by over 26% over the first five years of the forecast, total annual unrestricted state revenues from oil are projected to decrease by nearly 10%. Over the full ten years, total annual unrestricted state revenues from oil rise slightly, by 11%, by the end of the period. But that still pales in comparison to the more than 40% increase in annual production volumes over the same period. At those levels, the compound average growth rate for revenues is 1.1% (not even keeping pace with inflation), while that for production is 3.9%. Even looking at unrestricted annual oil revenues as a whole, that slight rise is hardly the commensurate increase promised by the proponents of SB21 in 2013 and 2014.

More importantly, when viewed as a share of gross wellhead revenues (net of royalty volumes), as demonstrated on the following chart, actual overall unrestricted state oil revenues decline over the period, from 19.25% at the beginning to 15.16% by FY31, before recovering slightly to 15.71% by the end.

Still others claim that the decline over the period is due to a shift in production from being almost entirely on state lands, from which the state receives royalties, to a mix that includes substantial volumes from federal lands, on which the state does not receive royalties.

But that argument also doesn’t hold. As the above chart shows, overall unrestricted state revenues from oil decline as a share of gross wellhead revenues, even after excluding royalties. If the argument were valid, those at least would hold even, if not increase, as the amount of oil property and corporate income subject to tax increased with the expansion of production into NPRA.

All these numbers also show significant decreases compared to those from the previous decade, the first under SB21.

As shown on the following chart, in the first decade under SB21, production tax revenues as a share of gross wellhead revenues (the red line) nearly doubled, rising from 3.32% in FY2016 to 6.68% in FY2025, with a median effective tax rate of 6.36% over the period.

Compared to those results, over the next ten years, the effective tax rate is projected to plunge from 5.46% at the beginning of the period to 3.43% by the end, with a median effective tax rate over the period of 3.43%, about half of the effective tax rate during the previous ten-year period.

Total state revenues as a share of gross wellhead revenues and total state revenues excluding royalties as a share of gross wellhead revenues also plunge between the two periods.

As shown in the chart above, over the first decade, total unrestricted annual state revenues (the dark blue line) averaged 20.53% of gross wellhead revenues (median); however, over the period from FY2026 through FY2035, state revenues are projected to average only 15.71% of gross wellhead revenues (median). Over the first decade, total unrestricted annual state revenues excluding royalties (the gold line) averaged 9.5% of gross wellhead revenues (median); over the period from FY2026 through FY2035, however, total state revenues excluding royalties are projected to average only 6.9% of gross wellhead revenues (median).

What is causing the decline?

As we have explained in previous columns, the cause is largely due to the stacking of preferential treatment for the so-called Gross Value Reduction (GVR) volumes on top of other production tax incentives (e.g., immediate expense deductions, per-barrel credits, carryover provisions, corporate-level calculation) already provided by SB21.

As explained in the Fall 2025 Revenue Sources Book (Fall 2025 Forecast), GVR treatment applies to production from “newly developed units, as well as certain new producing areas or expansion of producing areas.”

GVR preferences occur in two ways. First, gross revenue from production from GVR-eligible fields is entitled to a 20% to 30% exclusion from the production tax calculation. That means if a field eligible for GVR treatment is otherwise producing $100 million per day in gross wellhead revenue, only $70-$80 million of that revenue is subject to production tax. The producer retains the remaining $20-$30 million in revenue free of production tax.

Second, the “Per-Taxable-Barrel Credits for Gross Value Reduction (GVR) Production” available under SB 21 can be used to reduce tax below the Minimum Tax Floor.

As shown in the Department of Revenue’s recent analysis of Santos’ new Pikka project, those credits can eliminate production taxes entirely for up to seven years.

Because the level of production qualifying for GVR treatment was negligible in prior periods, the impact of the provisions on production tax revenues also was negligible. That changes over the next ten years, however.

Based on the Fall 2025 Forecast, GVR volumes are projected to jump from 3% of overall production to 35%.

The increase, particularly the rise in barrels generating credits not subject to the Minimum Tax Floor, is wreaking havoc on projected production tax revenues and, by extension, on overall unrestricted state oil revenues. While producers are projected to realize significant increases in gross wellhead revenues due to higher production, the state is projected to see its share of those revenues fall precipitously.

Rather than the outcome promised in 2013 and 2014, the Spring Forecast reaffirms that the opposite is occurring: increased production, particularly of GVR volumes, is causing significant reductions in state production tax revenues.

In previous columns, we have suggested responding to this situation by replacing the state’s multi-layered, overly complex production tax code, which causes the problem, with a simple, straightforward approach based on a percentage of gross wellhead revenues. As we have explained there, consistent with the promises made in 2013 and 2014, such an approach would ensure that, as production levels, and with them, gross wellhead revenues rise, so commensurately would state revenues.

Data from the Spring Forecast confirm this is the correct direction. Rather than the projected results under the current version of SB 21, here is what production tax revenues would look like if calculated over the next decade at a simple rate of 6.4% of gross revenues (the same as the median level from the last decade). Consistent with the promises made in 2013 and 2014, production tax revenues, and with them, overall state revenues from oil, would generally grow commensurate with the growth in production volumes.

Some suggest that changing the state’s production tax approach could undermine continued investment in Alaska oil production. They point, for example, to the results from this week’s sale of federal leases in NPRA and assert that the results would not have been the same under a simplified oil tax code.

But those bidding on the leases know that oil taxes are always subject to change and are aware that the current tax structure under SB 21 is already under review.

Moreover, under Article 8, Section 2 of the Alaska Constitution, the state is mandated to “provide for the … development … of all natural resources … for the maximum benefit of its people.” Clearly, a situation in which the state’s share of revenues falls precipitously as production increases is questionable under that standard. Reasonable investors should not anticipate the state to remain inactive in such a situation.

The fact that the bidding in NPRA remained strong despite that knowledge suggests that potential investors are undeterred by potential changes to the state’s oil tax code. Rather than supporting the claims by some that the current oil tax code should remain as is, the bids demonstrate that Alaska remains an attractive investment opportunity despite potential upcoming changes to the code.

As we explained in a previous column, Alaska needs to reform its oil tax approach now, before additional production volumes slip away under-taxed or, in the case of GVR volumes, left untaxed entirely. This is not a case where taxes are being deferred and will be recaptured later. Especially with the GVR volumes, this is a case where revenues will remain uncollected permanently.

The Spring Forecast confirms that, through its inaction, the Legislature continues leading Alaska in this direction.

Brad Keithley is the Managing Director of Alaskans for Sustainable Budgets, a project focused on developing and advocating for economically robust and durable state fiscal policies. You can follow the work of the project on its website, at @AK4SB on Twitter, on its Facebook page or by subscribing to its weekly podcast on Substack.

Oil tax reform might be back on the table if we get a better governor.

Good report. Thanks