In a recent news article in the Kenai Peninsula Clarion (“Alaska House candidates trade views at forum”), Justin Ruffridge, a Republican who is running to represent House District 7, is quoted as saying this:

Ruffridge said he was persuaded by a recent article out of the Alaska policy working group, which found that Alaska’s small population would require high income tax rates to provide sufficient state income. Any new sales tax, he said, could negatively impact state municipalities who already collect their own sales tax.

“No new taxes in this state will fix the problem,” Ruffridge said.

The “recent article” referenced in Ruffridge’s response is a repost by the Alaska Policy Forum of a recent analysis published by the Tax Foundation, a self-styled Washington, DC “think tank” described as “slightly to moderately conservative in bias.” Other than republishing it on an Alaska-based website, the Alaska Policy Forum repost referenced by Ruffridge doesn’t add anything to the Tax Foundation’s original version of the report (“Economic Implications of an Alaska Income Tax or Its Alternatives”), which is published here.

The report does not support the “no new taxes” claim made by Ruffridge.

The report focuses largely on a comparison of the economic impact of a state personal income tax compared to a state sales tax. It does not compare either to the economic implications of cuts in Permanent Fund dividends (PFDs) – what former Governor Jay Hammond referred to in his book, Diapering the Devil, as “reversibly graduated head taxes” and the funding approach that, in the real world faced by Alaskans, currently is being used to supply additional revenues to state government.

Indeed, in its entirety the report mentions the PFD only once, and then only in passing.

As we’ve explained previously, in the real world the reason the state needs new taxes is to substitute for the use of PFD cuts/”head taxes,” not to increase spending. And in that real world context, new taxes are a positive for the Alaska economy, not the negative claimed by Ruffridge.

As a 2016 report by economists at the University of Alaska-Anchorage’s Institute for Social and Economic Research (“ISER”) makes clear, of all of the revenue options the economists studied – including both the income and sales taxes covered in the Tax Foundation report, as well as PFD cuts and a statewide property tax – PFD cuts/”head taxes” have “the largest adverse impact on the [Alaska] economy per dollar of revenues raised.”

In the real world, replacing the existing approach that has the “largest adverse impact on the economy” with a different, lower impact tax approach would improve the economy, it would not make it worse.

Some argue that Ruffridge’s claim is correct because, in their view, the budget can be balanced without the need for either PFD cuts/”head taxes” or any other form of taxes – in other words, without additional revenue of any kind. Thus, any tax, whether the PFD cut/”head tax” or any approach is unnecessary.

But that’s not true in the real world. Governor Mike Dunleavy (R – Alaska) set out to accomplish that very goal in the 2019 legislative session, his first, and has failed spectacularly. As we explained in a previous column, not only has he failed to reduce the budget to the point where it balances without the need for additional revenues, over the course of his four year term the budget – and the resulting deficits – have actually increased. To close those deficits, the need for additional revenues has grown even greater over his time in office, not less.

The future does not look any different. This, from our most recent Friday “Goldilocks” charts, is our latest look at where the state is headed over the next ten years based on current futures prices for oil, the most recent projections of the percent of market value (POMV) draw and PFD from the Permanent Fund Corporation and an updated spending projection based on the actions of the legislature and governor this past session, adjusted for current market expectations of future inflation rates.

The red above the line indicates the level of deficits – put differently, the need for additional revenues – under current law (statutory PFD). Over the 10-year period, net deficits – the need for additional revenues – total $13.2 billion, or about $1.3 billion per year on average.

While substituting Governor Dunleavy’s proposed POMV 50/50 PFD for current law – which raises about $800 million per year on average over the period in new revenue – reduces the level of the deficits (and even produces surpluses – red below the line – in the first two years), it doesn’t come close to eliminating them.

Even using POMV 50/50 to increase revenues, over the 10-year period, net deficits – the need for additional revenue – still total $5.1 billion, or about $500 million per year on average.

Ruffridge’s claim “that Alaska’s small population would require high income tax rates to provide sufficient state income” is also incorrect.

Tax rates depend entirely on the revenue requirement, tax base and tax approach being used. The average tax rate is the quotient of dividing the revenue requirement (deficit) by the tax base. If the revenue requirement is 4 and the tax base is 40, the average tax rate is 10%; if, on the other hand, the revenue requirement is 2 and the tax base is 100, the average tax rate is only 2%.

The tax rate is also affected by the tax approach. A progressive approach increases the tax rate for the wealthiest above the average rate, and reduces the tax rate for those further down the income scale below the average rate. A regressive approach does the opposite. In either event, the marginal tax rates are above the average rate.

A proportional (or flat) approach does neither, applying the same (average) rate to all income brackets.

The Tax Foundation’s conclusions about an income tax are the result of vastly overstating Alaska’s real world revenue requirement – at one point they assume an annual revenue requirement of $4.7 billion versus a real world requirement of around $1.3 billion (or $500 million using POMV 50/50) – using a relatively narrow base and a progressive approach. As a result, the marginal tax rates they cite are substantially exaggerated.

As we’ve explained in a previous column, by using the real world revenue requirement, broadening the base and using a flat tax approach, the rates required to balance Alaska’s budget are, in fact, substantially lower not only than those referenced in the Tax Foundation report, but also the marginal rates used in other states.

Here’s where Alaska (in red) would fall compared to other states using a broad-based flat rate tax approach, near the very bottom of the scale.

By relying blindly on the Tax Foundation’s substantially inflated conclusions, Ruffridge’s comments fail to take those real world facts into account.

The Tax Foundation’s report also does not include a distributional analysis comparing “who pays” under the approaches it evaluates.

While it admits that sales taxes “can be regressive,” the report asserts that “broader bases that include consumer services (much more heavily consumed by higher-income individuals) push in a progressive direction.”

That’s true only to a point, however. By definition, sales taxes automatically exclude the portion of income saved or invested, which generally rises with income level. Thus, even if broadly applicable to sales of both goods and services, sales taxes still tilt more heavily against middle and lower income families than other options.

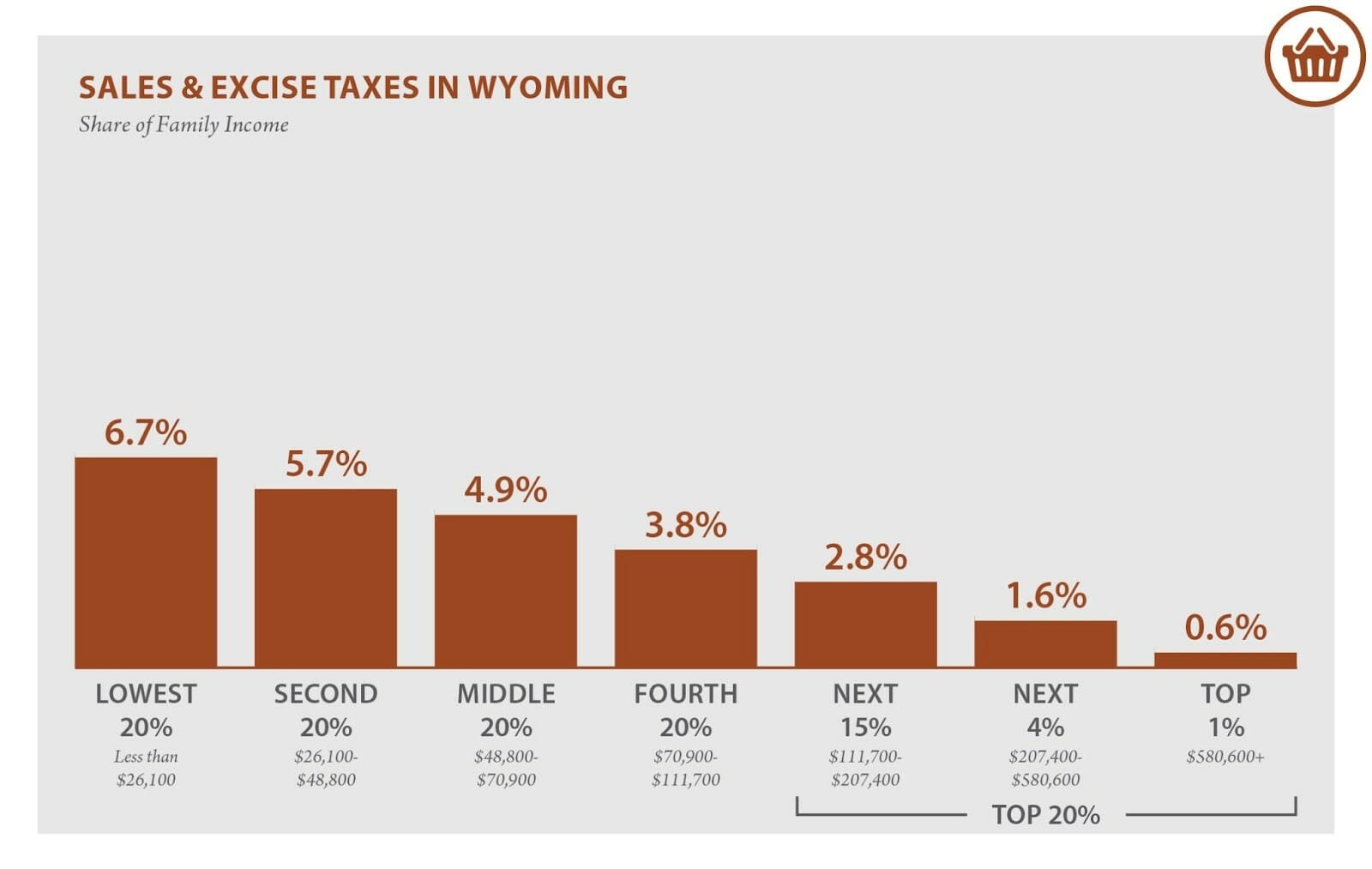

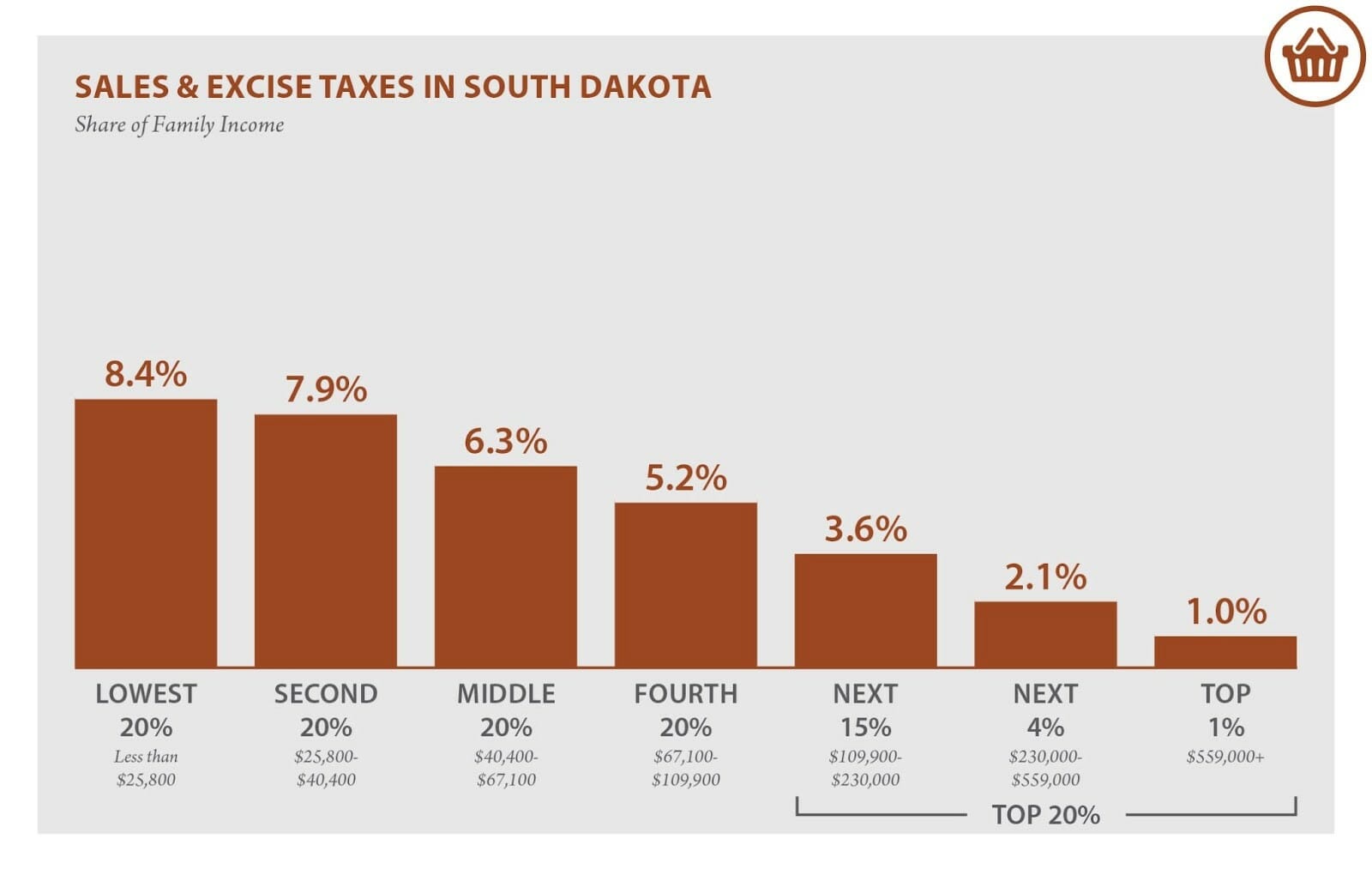

This can be seen by looking at the distributional impact of the Wyoming and South Dakota sales taxes, which currently are number 1 and 2 in the Tax Foundation’s most recent ranking of the “State Business Tax Climate,” and which both generally apply to both goods and services.

According to the Institute on Taxation and Economic Policy’s (ITEP) most recent, state-by-state “Who Pays” analysis, here’s the distributional impact of sales taxes in each state (the Tax Foundation does not appear to do a distributional analysis of sales taxes):

Even though they both apply broadly to both goods and services, both remain significantly regressive, taking increasingly more from middle and lower lower income families than from those in the top 20%. In Wyoming, middle income families pay more than eight times, and the lowest 20% more than 11 times of their income in sales taxes than those in the top 20%. In South Dakota the corresponding numbers are more than six times and more than eight times.

It is because of this significantly regressive impact that a 2017 ISER study concludes that, in Alaska, a statewide sales tax would be the “next costliest [revenue measure, after only PFD cuts] for households with children,” and why we previously have labeled it as the top 20% “fall back plan” if PFD cuts are rejected.

By failing to compare the impact of taxes against the real world economic impact of continued and deepening PFD cuts, the Tax Foundation report Ruffridge relies on does not provide the support he thinks it does. It is starkly silent on the real world choices that face Alaska lawmakers.

Because Ruffridge’s “no new taxes” approach would keep PFD cuts/”head taxes” in place, his position would leave Alaska limping along using the funding approach that has the “largest adverse impact” on its economy, rather than adopting a lower impact alternative. His position also would condemn middle and lower income – 80% of – Alaska families to continue to bear the brunt of providing the additional funds undeniably required in the real world to balance the Alaska budget in the years ahead.

Even if Ruffridge followed the Tax Foundation’s advice and proposed using a sales tax to fill the state’s continuing deficits, he still would be siding with the top 20% against middle and lower income Alaska families. While not as regressive as PFD cuts, as the Wyoming and South Dakota experiences demonstrate, even at their broadest sales taxes still would push the bulk of the burden disproportionately to the “bottom 80%” of Alaska families.

In the real world, Alaska’s choice going forward isn’t taxes v. no taxes, it’s what kind of taxes Alaska families will pay. By rejecting other, lower impact and more equitable options, Ruffridge’s answer appears to be PFD cuts/”head taxes,” the approach that has the “largest adverse impact” on 80% of Alaska families and the overall Alaska economy. That’s not acceptable.

Brad Keithley is the Managing Director of Alaskans for Sustainable Budgets, a project focused on developing and advocating for economically robust and durable state fiscal policies. You can follow the work of the project on its website, at @AK4SB on Twitter, on its Facebook page or by subscribing to its weekly podcast on Substack.

Thank you for your efforts to push equity to the forefront as we debate our state budget challenges.

At some point I’d like to see an analysis of the value of the services we’re gifting to Outside & foreign entities/investors as a result of our (non) tax policies. This seems worthy of examination given that 65-70% of the cost of those services comes from a trust fund dedicated to the welfare of Alaskans, and a large slice of the remainder comes from similarly-dedicated natural resources.

A resident of another state or country merely has to start up a business or invest here, and legislators & state officials will crawl out of the woodwork on Day One and start shoveling cash from the Permanent Fund into his bank account. Those of us who actually live here, meanwhile, have to file an annual application and sign it under penalties of perjury to harvest our measly annual benefit from the same pot of money. We could easily build a database to define the extent of this problem by inviting all businesses & investors, local and foreign, to file… Read more »

Just wondering if the State has collected the past due amount of taxes from the pot industry. My guess is no.

So what Brad is saying is Alaskans should give away our oil like a banana republic and Alaskans should subsidize the giveaway of our oil through income taxes and sales taxes. Sure. That sounds fair. Alaskans subsidizing the likes of Exxon, ConocoPhillips, et al.

BS.